Global Pharmaceutical Packaging Market Strategic Analysis 2024

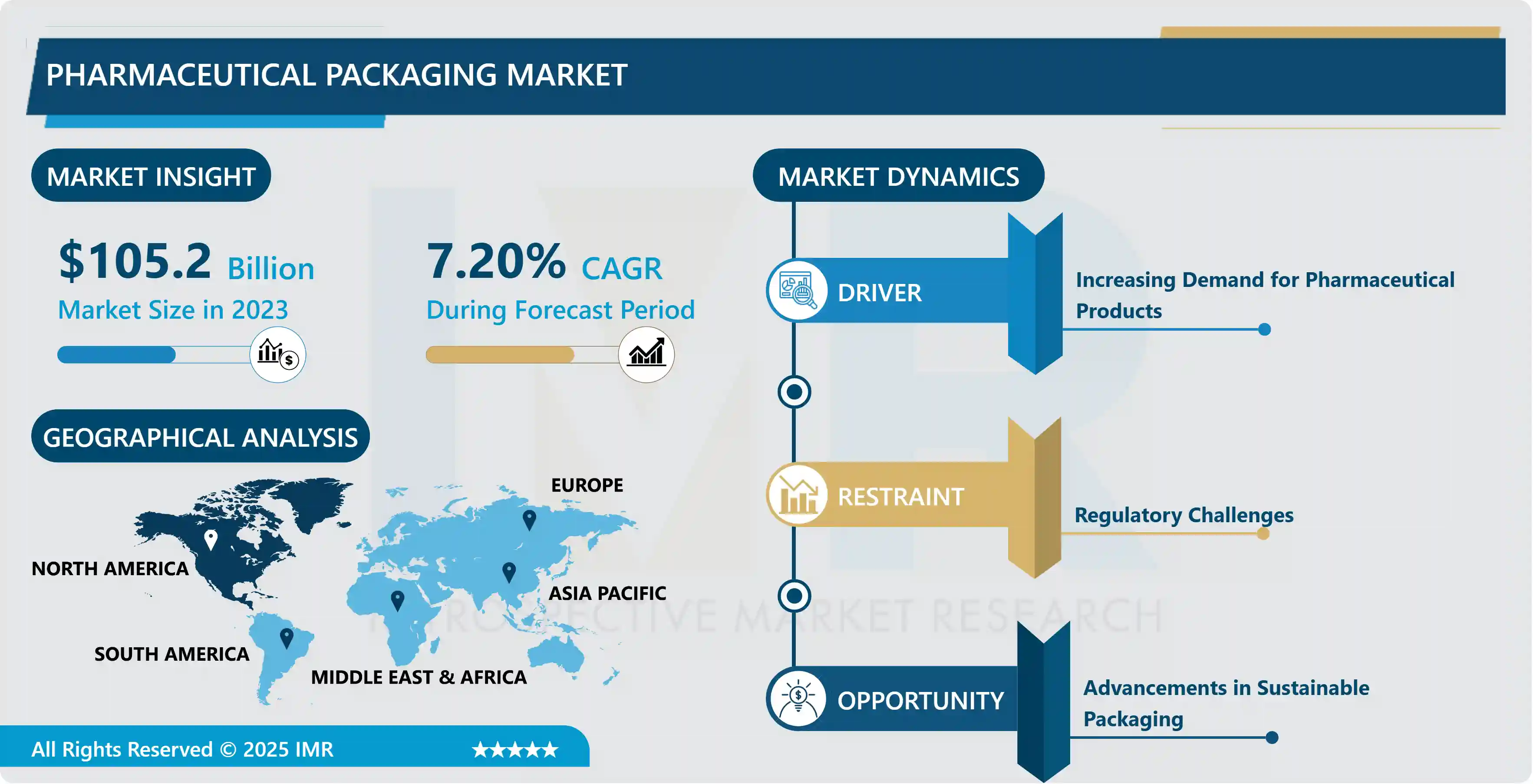

The Global Pharmaceutical Packaging Market Size Was Valued at USD 105.2 Billion in 2023 and is Projected to Reach USD 196.7 Billion by 2032, Growing at a CAGR of 7.2% From 2024-2032.

Pharmaceutical packaging refers to the specialized materials and processes used to enclose, protect, and identify pharmaceutical products throughout their lifecycle. This critical component of the healthcare industry ensures that medications remain stable, sterile, and safe from environmental contaminants, physical damage, and counterfeiting. The market encompasses a wide range of primary packaging (blister packs, bottles, vials, ampoules), secondary packaging (cartons, boxes), and tertiary packaging, all of which must comply with rigorous global regulatory standards to ensure patient safety and product efficacy.

The primary advantage of advanced pharmaceutical packaging over traditional methods is the integration of "smart" and active technologies that enhance shelf-life and patient compliance. Modern solutions include child-resistant features, tamper-evident seals, and temperature-controlled materials that are essential for the global distribution of biologics and vaccines. Major sectors within the healthcare industry utilizing these solutions include pharmaceutical manufacturers, contract packaging organizations (CPOs), and research laboratories. The rising global demand for generic drugs, coupled with the rapid growth of the biopharmaceutical sector, is a significant driver of the market’s robust expansion.

👉 To request a sample report: https://introspectivemarketresearch.com/request/18462

Market Segmentation

The Pharmaceutical Packaging Market is segmented into Type, Material, and End-Use. By Type, the market is categorized into (Primary Packaging, Secondary Packaging, Tertiary Packaging). By Material, the market is categorized into (Plastics & Polymers, Glass, Paper & Paperboard, Metals). By End-Use, the market is categorized into (Pharma Manufacturing, Contract Packaging, Retail Pharmacy, Institutional Pharmacy).

Growth Driver

The principal growth driver for the Pharmaceutical Packaging Market is the rapid global expansion of the biopharmaceutical sector, particularly the production of specialty drugs and vaccines. These complex biological products are highly sensitive to environmental factors such as light, temperature, and oxygen, requiring sophisticated primary packaging solutions like pre-fillable syringes and advanced vials. Additionally, the ongoing global push for standardized serialization and track-and-trace technologies to combat the rise of counterfeit medicines is forcing manufacturers to invest in high-tech packaging solutions. This regulatory pressure, combined with the increasing volume of chronic disease treatments, ensures a steady rise in demand for secure packaging.

Market Opportunity

A major market opportunity exists in the development of sustainable and eco-friendly packaging materials. As environmental regulations tighten and corporate social responsibility becomes a priority, the industry is seeking alternatives to single-use plastics and non-recyclable laminates. The innovation of bio-based polymers and recyclable paperboard systems that maintain high barrier properties offers a transformative potential for market leaders. Furthermore, the rise of "Smart Packaging" incorporating NFC tags or QR codes to track dosage and provide patient education—represents a high-growth niche that aligns with the digital transformation of modern healthcare.

Detailed Segmentation

Title: Pharmaceutical Packaging Market Market, Segmentation The Pharmaceutical Packaging Market is segmented on the basis of Type, Material, and End-Use.

Type

The Type segment is further classified into Primary Packaging, Secondary Packaging, and Tertiary Packaging. Among these, the Primary Packaging sub-segment accounted for the highest market share in 2023. Primary packaging, which includes blister packs, bottles, and vials that come into direct contact with the medication, is the most critical segment due to its role in preserving chemical stability and sterility. The dominance of this segment is driven by the high volume of oral solids and injectable drugs produced globally. As the industry shifts toward more complex drug delivery systems, the demand for specialized primary containers that offer superior barrier protection and compatibility with active ingredients continues to be the primary driver of market value.

Material

The Material segment is further classified into Plastics & Polymers, Glass, Paper & Paperboard, and Metals. Among these, the Plastics & Polymers sub-segment accounted for the highest market share in 2023. Plastics remain the dominant material choice due to their exceptional versatility, light weight, and cost-effectiveness. High-density polyethylene (HDPE) and polypropylene are widely used for bottles and closures, while PVC and PCTFE are essential for blister packaging. The material’s ability to be molded into various shapes while providing adequate protection against moisture and air makes it the standard for both over-the-counter and prescription medications across all global regions.

Some of The Leading or Active Market key Players Are-

Amcor plc (Switzerland) Becton, Dickinson and Company (United States) Gerresheimer AG (Germany) Schott AG (Germany) West Pharmaceutical Services, Inc. (United States) Berry Global Group, Inc. (United States) AptarGroup, Inc. (United States) Catalent, Inc. (United States) SGD Pharma (France) Nipro Corporation (Japan) CCL Industries Inc. (Canada) WestRock Company (United States) and other active players.

Key Industry Developments

In May 2024, Amcor plc announced the launch of a new recycle-ready blister pack solution. This innovation addresses the long-standing challenge of recycling multi-material medicine packs by using a mono-material structure that maintains the high barrier protection required for sensitive medications. This development is expected to set a new benchmark for sustainability in the primary packaging sector.

In January 2024, Gerresheimer AG expanded its production capacity for glass vials and pre-fillable syringes in North America. This strategic investment was made to support the growing demand for injectable biologics and GLP-1 medications. By utilizing advanced automation and cleanroom technology, the company aims to provide high-purity glass solutions that meet the specialized needs of the rapidly growing biopharmaceutical market.

Key Findings of the Study

· Dominant Segments: Primary Packaging and Plastics & Polymers currently lead the market in terms of revenue and manufacturing volume.

· Leading Regions: North America maintains the largest market share, supported by a massive pharmaceutical R&D hub and stringent FDA packaging regulations.

· Key Growth Drivers: The rise in chronic diseases and the increasing global requirement for anti-counterfeiting serialization are the primary catalysts.

· Market Trends: There is a significant shift toward "Green Packaging" and the integration of IoT-enabled smart labels to improve patient adherence and supply chain transparency.

🔍 𝐈𝐧-𝐃𝐞𝐩𝐭𝐡 𝐑𝐞𝐩𝐨𝐫𝐭:

https://introspectivemarketresearch.com/reports/pharmaceutical-packaging-market/

About Introspective Market Research

Introspective Market Research is a global provider of data-driven market intelligence and strategic advisory services. Our analysts and consultants deliver comprehensive reports, actionable insights and customized consulting to clients across chemicals & materials, healthcare, energy, environment, infrastructure, and advanced manufacturing sectors.

Media Contact:

Introspective Market Research.

Email: press@introspectivemarketresearch.com

Website: http://www.introspectivemarketresearch.com

Phone: +91-91753-37569